No products in the cart.

Think of backpacker travel insurance as the Swiss Army knife in your travel kit. It’s that one piece of gear you pack hoping you’ll never have to use it, but if you do, you'll thank your lucky stars you have it. This isn't your standard vacation insurance; it's a different beast entirely, built from the ground up for long-term, unpredictable journeys that might span several countries.

Why Backpacker Insurance Is Your Most Essential Gear

Standard vacation insurance is like a pair of flip-flops—great for a week at a beach resort, but completely out of its depth on a six-month trek through the Andes. It's designed for fixed dates, a single destination, and short trips. Travel insurance for backpackers, on the other hand, is the pair of sturdy, broken-in hiking boots made for the long haul.

It’s a specialized safety net, custom-built for the spontaneous and adventurous nature of backpacking. This kind of policy understands that your plans are written in sand, not stone. It knows you’re more likely to be in a hostel than a five-star hotel, and that you might impulsively decide to go rock climbing in Thailand one week and scuba diving in Vietnam the next.

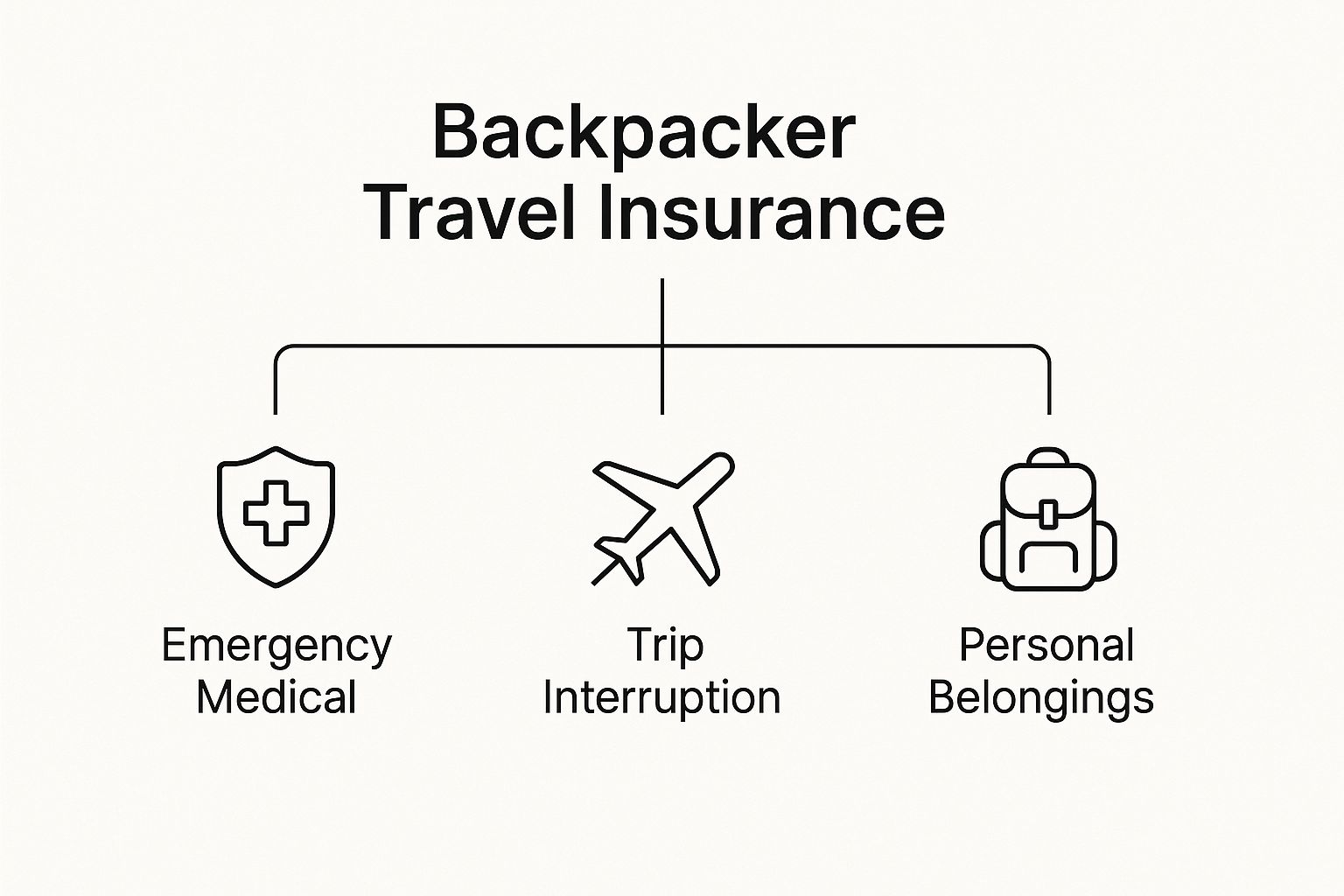

More Than Just Medical Emergencies

While getting you patched up after an accident is the absolute core of any good policy, true backpacker insurance protects your entire journey. It's a comprehensive shield that anticipates the unique risks that come with living out of a backpack.

This infographic gives a great overview of the main pillars of coverage.

As you can see, it goes way beyond just hospital bills, covering everything from cancelled flights to stolen gear.

The need for this kind of flexible protection has exploded. By 2025, the global travel insurance market hit a value somewhere between $22.1 billion and $30.77 billion, largely because we've all become more aware of the things that can go wrong. The surge is especially strong among younger travelers who are choosing long-term, adventurous trips and need insurance that can keep up.

A common mistake is to see insurance as just another expense to tick off the list. The right way to look at it is as an investment in your own freedom. It's the confidence to say "yes" to that impromptu trek or last-minute flight, knowing you've got a solid backup if things sideways.

Getting into this mindset is a game-changer, especially if you're new to this. If you’re at the very beginning of your planning, our guide on backpacking for beginners is packed with essential tips to get you started on the right foot.

Of course, a good insurance policy is just one piece of the puzzle. For a complete checklist on how to prepare for international travel—covering everything from documents to finances—this resource is invaluable. It’s all about building layers of security so you can focus on the adventure, not the "what-ifs."

Understanding Your Core Insurance Coverage

Let's cut through the jargon. At its heart, backpacker travel insurance is built on a foundation of a few critical protections. Think of them as the pillars supporting your entire trip—if one is missing, things can get wobbly, fast.

Getting a handle on these core components is the first step to seeing insurance not as a complex legal document, but as a practical, essential piece of your travel gear. We'll break down each one with real-world scenarios you can actually picture yourself in.

The Lifeline of Emergency Medical Coverage

This is the big one. The absolute, non-negotiable foundation of any good policy. It’s designed to cover the costs of accidents and illnesses abroad, from a quick doctor's visit for a stomach bug to a major hospitalization. Without it, a simple mishap could spiral into crippling debt.

Imagine you're trekking in a remote national park, miles from the nearest town. You slip on a loose rock, and a sharp, sickening pain shoots up your ankle. It’s clearly broken, and you can't walk. This is precisely when emergency medical coverage kicks into gear.

It doesn’t just pay the doctor; it orchestrates your entire rescue. A solid policy will cover:

- Emergency Evacuation: The cost to get you from that remote trail to a proper hospital. This can involve helicopters or specialized vehicles and easily run into thousands of dollars.

- Hospitalization: All your medical bills, from the initial surgery to your hospital stay and follow-up care.

- Repatriation: In a worst-case scenario, this covers the cost of flying you back to your home country for further treatment if it’s medically necessary.

This kind of coverage is paramount. Recent industry data shows that travel medical insurance, including hospitalization and emergency evacuation, now features in over 70% of all travel insurance sales. It's a clear sign that travelers are more aware than ever of potential health risks abroad.

Trip Interruption: Your Financial Safety Net

Life doesn't stop just because you're on the road. Trip interruption coverage acts as your financial parachute when a serious emergency back home forces you to cut your trip short. It's there to reimburse you for the unused, non-refundable parts of your journey.

Let's say you’re three months into a six-month adventure across Southeast Asia. You’ve already booked several flights, tours, and hostels for the coming weeks. Then, you get a sudden call about a family emergency and have to fly home immediately.

Without insurance, all the money you spent on those future bookings would simply be gone. With trip interruption coverage, you can file a claim to get back the cost of your unused flights, accommodation deposits, and pre-paid tours. It turns a potential financial disaster into a manageable situation.

Protecting Your Gear with Personal Belongings Coverage

When you're backpacking, your pack is your entire world on your shoulders. It holds your clothes, your tech, your documents—everything. Personal belongings coverage is designed to help you replace that essential gear if it gets stolen, lost, or damaged.

Picture this: you’re on an overnight bus, and you doze off. When you wake up at your destination, your daypack—the one with your laptop, passport, and camera—is gone. It’s a gut-wrenching feeling that can stop a trip in its tracks.

This coverage is designed for that exact moment. While policies have limits, it provides the funds you need to replace your stolen items and get back on your feet. You'll need a police report, but it’s a crucial buffer against the all-too-common risk of theft. The same coverage often applies if an airline loses your main backpack.

This focus on core protections reflects a shift in the market. While single-trip policies still make up 61.3% of the U.S. market, long-stay and annual plans are gaining ground, now capturing 38.7%—a clear nod to the growing number of backpackers and long-term travelers. You can learn more about these travel insurance trends and insights on battleface.com.

Personal Liability: When You're at Fault

This is the often-overlooked hero of travel insurance. Personal liability protects you if you accidentally injure someone else or damage their property. It might sound unlikely, but simple accidents can lead to huge legal and financial headaches.

Here’s an everyday example: you rent a scooter to explore an island. You take a corner a bit too fast and clip a parked motorcycle, leaving a large, expensive-looking scratch. The owner is furious and demands you pay for the repairs on the spot.

Your personal liability coverage can step in to cover these costs, preventing a minor accident from escalating into a major conflict or a demand for a huge sum of money you simply don't have. It's peace of mind for the unexpected consequences of your own actions.

To pull it all together, here is a quick-glance table breaking down these essential coverages.

Essential Backpacker Insurance Coverage Breakdown

| Coverage Type | What It Covers | Why It's Essential for Backpackers |

|---|---|---|

| Emergency Medical | Hospital stays, doctor visits, surgery, ambulance transport, and emergency evacuation. | Covers massive, unexpected medical bills in foreign countries. Essential for remote trekking or adventure sports. |

| Trip Interruption | Reimburses non-refundable costs if you have to end your trip early due to a covered reason (e.g., family emergency). | Protects the thousands you may have pre-paid for flights and tours, saving you from a huge financial loss. |

| Personal Belongings | Reimbursement for stolen, lost, or damaged gear like laptops, cameras, passports, and clothing. | Your backpack holds everything you need. This helps you replace essential items quickly after theft or loss. |

| Personal Liability | Covers legal fees and costs if you accidentally injure someone or damage their property. | A simple mistake (like a scooter accident) could lead to enormous costs. This protects your finances from mishaps. |

Ultimately, a good backpacker policy is about having these four pillars firmly in place, giving you the confidence to handle whatever the road throws at you.

Getting Coverage for Adventure Sports

Let’s be honest, backpacking and adventure go hand in hand. You might be planning to hike a mountain pass, explore a reef, or just rent a quad bike for the afternoon. These are the stories you'll tell for years. But here’s the reality check many travelers miss: your standard travel insurance for backpackers might see these incredible moments as unacceptable risks.

In the language of insurance, anything that bumps up your chances of getting hurt is often labeled an “adventure sport” or “hazardous activity.” This isn’t just about extreme stuff like bungee jumping, either. Even activities that feel pretty tame, like a day hike, kayaking, or riding a scooter, can fall under this umbrella and get you denied coverage.

Without the right policy, one bad fall on a jungle trek could leave you with a massive medical bill. It's a classic trap that catches even seasoned travelers off guard—discovering your insurance won't pay up because "hiking" was buried deep in the exclusions list.

Why Standard Policies Fall Short

Think of a basic insurance policy like a standard family car. It's perfect for driving around town on paved roads. But if you’re planning to go off-roading, you need the 4x4. That’s your adventure sports coverage. Standard plans are designed for low-risk travel, not the unpredictable nature of an adventure.

Insurers are all about statistics. They know which activities lead to more claims, and they either exclude them entirely or charge you more to cover them. This is why you have to get good at reading the fine print, especially the sections on exclusions and optional add-ons.

Before you buy any policy, do a quick "Ctrl+F" on the policy document for every single activity you plan on doing. Don't assume anything is covered, no matter how common it seems. If you can't find it, email the provider and get a straight answer in writing.

Finding the Right Adventure Coverage

So, how do you make sure your thirst for adventure doesn't leave you high and dry? You need a policy that actually matches your plans. Generally, you’ll find two main options.

- Policies with Built-in Adventure Coverage: Some companies, especially those that focus on travel insurance for backpackers, pack their standard plans with coverage for a long list of activities. These are fantastic if you're an all-rounder who might try a bit of everything.

- Policies with Optional Add-ons: Other insurers start with a cheaper, bare-bones plan and let you bolt on "sports and activities packs" for an extra fee. This can be a smart, budget-friendly move if you only have one or two specific high-risk activities on your list.

Lots of backpackers want to try popular adventure sports like scuba diving, so making sure your insurance is on board is non-negotiable. The same goes for things like rock climbing, which demands both the right coverage and the right gear. To get ready, take a look at our complete rock climbing gear checklist so you're prepared for a safe climb.

In the end, it’s a simple calculation. If your trip looks like a highlight reel of trekking, diving, and climbing, go for a comprehensive policy that includes adventure sports from the start. But if you’re mostly sticking to cities with just one big thrill planned, a simple add-on might be all you need.

Common Policy Exclusions You Must Know

Knowing what your travel insurance for backpackers covers is only half the story. The other, and arguably more important half, is understanding what it doesn't cover. This is where the fine print comes in—the land of exclusions, where a simple oversight can lead to a denied claim and a bill for thousands of dollars.

Think of your policy as a safety net. It's strong, but it has holes in it by design. Your job is to know exactly where those holes are before you even leave home. Honestly, overlooking these exclusions is one of the biggest mistakes a traveler can make, turning a minor hiccup into a trip-ending disaster.

So, let's pull back the curtain on the most common traps that catch even seasoned backpackers off guard.

The Impact of Alcohol or Drugs

This one is a biggie, and it's pretty much a universal rule. If you get hurt or lose something while under the influence of alcohol or non-prescribed drugs, you can almost guarantee your claim will be denied. Insurers see this as you taking an unnecessary risk, which effectively voids your coverage for that incident.

Picture this: you have a few beers at a full moon party and go for a swim. If you cut your foot on a rock, the insurer can request your medical report. If that report shows a high blood alcohol level, they have every right to refuse to pay for your stitches.

Undeclared Pre-existing Medical Conditions

When you're applying for a policy, total honesty is the only way to go. A pre-existing condition is any medical issue you’ve had symptoms of or been treated for before your insurance kicks in. This could be anything from asthma to a dodgy knee from a five-a-side football game.

If you don't declare it and it flares up on the road, the insurance company will almost certainly deny your claim. They'll dig into your medical history, and that undisclosed condition will be a massive red flag. Always declare everything; it’s better to pay a bit more for a policy that properly covers you than to have one that’s useless when you need it most.

Leaving Your Gear Unattended

This is a tough one for a lot of backpackers. Your coverage for personal belongings is only valid if you’ve taken "reasonable care" to protect them. Leaving your backpack on a chair in a cafe while you pop to the loo? That’s often seen as negligence.

Cautionary Tale: I've seen it happen. A traveler leaves their laptop bag on their train seat while they go to the buffet car. They come back, and it's gone. The claim is denied because the bag was left unattended in a public place. Your gear needs to be physically on you or secured in something like a locked hostel locker.

Understanding these exclusions is about understanding your side of the bargain. It's not just about paying for a policy—it's about following its rules.

Key Exclusions Checklist

Before you buy any travel insurance for backpackers, get absolutely clear on the fine print. Use this checklist to grill the provider:

- Reckless Behavior: What’s their specific definition of "reckless"? Ask for real-world examples. Does having two beers and twisting your ankle count?

- High-Risk Activities: We've touched on adventure sports, but get specific. Are there altitude limits for hiking? Depth limits for scuba diving?

- Illegal Acts: Your cover is toast if you’re injured while breaking local laws. A super common one in Southeast Asia is getting into a scooter accident without the right international license. Your home license often isn't enough.

- Working Abroad: Thinking of picking up some cash work? Most standard backpacker policies won't cover you for injuries you get while on the job, even if it's just a few bar shifts.

Of course, for the small stuff, you should be prepared to handle it yourself. Insurance is for emergencies, not for everyday scrapes. For tips on being self-sufficient, take a look at our guide on what to pack in a proper wilderness first aid kit.

How to Choose the Right Insurance Plan

Feeling swamped by all the options for travel insurance for backpackers? You’re not alone. It can feel like a maze, but if you break it down, you can find a plan that fits your trip perfectly without draining your travel fund.

Think of it like choosing a new backpack. You wouldn't just grab the first one you see. You'd check the size, how tough it is, and whether it’s comfortable enough for a long haul. Your insurance policy needs that same level of thought.

The trick is to tackle it step-by-step. By figuring out what you actually need and then comparing your options, you'll go from confused to confident.

Start With Your Unique Travel Style

Every backpacker’s trip is one of a kind, and so are their insurance needs. The first move is to map out the DNA of your adventure. This quick self-check is the key to finding a policy that truly has your back.

Just ask yourself a few simple questions:

- Where are you going? Medical care in the USA or Western Europe costs a whole lot more than in Southeast Asia. Your destination list is directly tied to how much medical coverage you’ll want.

- How long will you be away? Are you doing a three-month dash across a continent or planning a year-long, go-with-the-flow journey? You’ll want a policy that’s flexible and lets you easily add more time online if your plans change.

- What will you be doing? Is your trip all about museums and city cafes, or are you planning to go scuba diving, mountain trekking, and rock climbing? Your activities will tell you if you need to look for an adventure sports add-on.

- What are you packing? If you’re carrying a $1,500 laptop and a $1,000 camera, you need a policy with a high "single-item limit" for your electronics. A basic plan might only cover $500 per item, which would leave you seriously short if your gear gets stolen.

Your answers to these questions will create a personal checklist. This becomes your cheat sheet for instantly filtering out policies that don't fit and homing in on the ones that do.

Compare Providers Beyond the Price Tag

Once you know what you’re looking for, it’s time to start shopping. But here’s a pro tip: the cheapest policy is almost never the best one. The real value is buried in the details of the coverage, not just the initial quote.

When you’re comparing different travel insurance for backpackers, look past the price and focus on three crucial numbers:

- Coverage Limits: This is the absolute maximum an insurer will pay out for a certain type of claim. A $50,000 medical limit might sound like a lot, but a bad accident in some countries could blow past that in a heartbeat. Always aim for strong medical and emergency evacuation limits.

- Deductible: This is the amount you have to pay yourself before the insurance company steps in. A policy with a $250 deductible might be cheaper upfront, but you'll be on the hook for that first $250 of any claim.

- Customer Reviews: Don't just take the company's word for it. Jump on independent review sites like Trustpilot and see what actual travelers are saying. Pay special attention to comments about the claims process—a company that’s easy to work with when things go wrong is worth its weight in gold.

A smooth claims process is a must-have. Look for modern features like a mobile app for filing claims and 24/7 customer support. The absolute last thing you want is to be stuck fighting with a clunky website or waiting on hold from a noisy hostel halfway across the world.

The travel insurance world is also shifting. For a long time, Europe was the biggest market, making up 35–39% of the global share, partly because insurance is required for Schengen visas. But the fastest growth is now happening in the Asia-Pacific region, which is expected to grow by 15–16% in the coming years as more young travelers head to places like Bali and Vietnam. This global change means more competition and better options for backpackers everywhere. You can explore more about these travel insurance industry statistics on coinlaw.io.

Comparing Top Backpacker Insurance Features

To keep everything straight, it helps to lay out your top choices in a simple comparison table. This lets you see everything side-by-side, making it easier to pick a winner based on facts, not just a gut feeling.

| Feature | What to Look For | Why It Matters |

|---|---|---|

| Medical Limit | At least $100,000, but higher is better for expensive regions. | A serious medical emergency or evacuation can easily run up a six-figure bill. |

| Deductible | $0 to $250. A lower deductible means less out-of-pocket cost per claim. | A high deductible can make it not worthwhile to file smaller claims for stolen items or minor doctor visits. |

| Adventure Sports | A clear list of included activities or an affordable add-on pack. | Ensures you're covered for that spontaneous trek or dive without having to buy a separate policy. |

| Electronics Cover | A "single-item limit" that matches the value of your most expensive gear. | Prevents you from being underinsured if your expensive laptop or camera is stolen. |

| Flexibility | The ability to buy or extend a policy while already traveling. | Perfect for open-ended trips where your return date is unknown. |

By following a clear process like this, you take the mystery out of buying insurance. You’ll end up with a policy that not only fits your budget but gives you the solid protection you need to get out there and explore the world with real peace of mind.

Answering Your Top Insurance Questions

Let's be honest, diving into the world of travel insurance for backpackers can feel like trying to decipher a secret code. You get the general idea, but it's those specific, "what-if" scenarios that really throw you for a loop. These are the exact questions you hear whispered in hostel dorms and debated in travel forums.

To cut through the noise, we've rounded up the most common questions and laid out the answers in plain English. Think of this as your go-to guide for those tricky situations that the policy documents don't always make crystal clear.

Can I Buy Insurance After I've Already Started Traveling?

It's the classic backpacker nightmare. You've just landed, the adventure is starting, and a cold wave of panic washes over you—you forgot to buy insurance. The short answer is yes, you can usually get covered mid-trip, but it’s not as straightforward as buying it back home.

A handful of specialist insurers offer what’s called an “already traveling” or “on the road” policy. These plans almost always come with a catch designed to stop people from, say, breaking a leg and then buying a policy.

Most "already traveling" policies have a mandatory waiting period, often around 72 hours, before most of the coverage (especially for medical issues) kicks in. This means you’re not protected right away and are still exposed to risk for a few days.

Because you’re already out there, your options are much more limited and often more expensive. The smartest, simplest, and cheapest move is always to sort your insurance before you even leave for the airport. But if you’re in a pinch, look for providers who specifically advertise this feature.

How Do I Actually Make a Claim From the Road?

The thought of wrestling with paperwork while you're supposed to be relaxing in a hammock can be a major headache. Thankfully, most modern insurers have made this process surprisingly simple. The trick is to act fast and document everything.

What you do first really depends on how serious the situation is.

- For a Major Emergency: If you’re seriously sick or injured, your first and only priority should be to call your insurer's 24/7 emergency assistance line. Don't hesitate. They’ll guide you, approve medical treatments, and even deal with the hospital directly.

- For Non-Emergencies: If your camera gets stolen, your first stop is the local police station. You need to file a report, typically within 24 hours of the incident. This official report is the one piece of paper you absolutely need for any theft claim.

Once you’ve taken those initial steps, the rest of the claim is usually handled online. You'll fill out a form on the insurer's website or app and upload photos of your documents—like that police report, medical receipts, or proof of ownership for stolen items. Keeping digital backups of everything will make your life so much easier.

Is My Expensive Camera or Laptop Actually Covered?

Yes, your tech is generally covered, but this is where you really have to read the fine print. It’s one of the biggest traps for backpackers, who often assume their expensive gear is fully protected when it’s not.

You need to hunt down two key numbers in your policy:

- Single-Item Limit: This is the absolute maximum the insurer will pay for any one item, no matter what it's actually worth. A standard policy might cap this at just $500. If your $1,500 laptop gets swiped, you’ll only get that $500 back.

- Total Valuables Limit: This is the maximum they'll pay out for all your valuable items combined.

If you’re traveling with a nice camera, a drone, or a powerful laptop, you can't afford to overlook this. You'll need to find a policy with higher limits from the get-go or buy a specific "gadget" add-on to cover your electronics properly. Don't just cross your fingers and hope for the best—check the numbers before you buy.

What if My Trip Is Open-Ended and I Have No Return Date?

Ah, the true spirit of backpacking! This is exactly what separates a real travel insurance for backpackers policy from a standard two-week vacation plan. The best policies are built for this kind of freedom and flexibility.

You'll want to look for a plan that doesn't force you to lock in a return date. Many of the top providers let you buy an initial block of time—say, six months—and then give you the option to extend it online as your adventure continues.

This allows your insurance to follow your journey, not the other way around. Just make sure you check the maximum duration you can be covered for in total. Most policies have an upper limit, whether it's 12, 18, or even 24 months. For anyone chasing an open-ended adventure, this flexibility is non-negotiable.

At FindTopTrends, we know that having the right gear is just as important as having the right insurance. From bombproof backpacks to the tech you need to capture incredible memories, we've curated the best trending products to make your trip smoother, safer, and more fun.

Ready to gear up? Explore our collection of top-rated travel essentials.

Leave a comment