No products in the cart.

Unlocking Your Family's Financial Future: A Practical Guide

Managing household finances can feel like navigating a complex maze, especially with the ever-changing needs of a growing family. From daily expenses and school supplies to saving for college and retirement, the financial pressures are real and constant. The good news is that achieving financial stability and peace of mind is entirely within your reach. Effective money management isn't about restriction; it's about empowerment.

This guide is designed to provide powerful and practical budgeting tips for families, moving beyond generic advice to offer actionable strategies you can implement today. We will explore seven proven methods, each tailored to different family dynamics and financial situations. You will learn specific techniques like the 50/30/20 Rule for categorizing spending, Zero-Based Budgeting for total control, and the tangible Envelope Method for managing cash flow.

We'll also cover proactive strategies such as paying yourself first to prioritize savings and holding regular family budget meetings to ensure everyone is on the same page. Whether you're just starting your family, navigating the teen years, or planning for long-term goals, these tips will equip you with the tools to build a secure financial foundation, reduce stress, and work together toward your shared dreams. Let’s dive into the strategies that can transform your family's financial well-being.

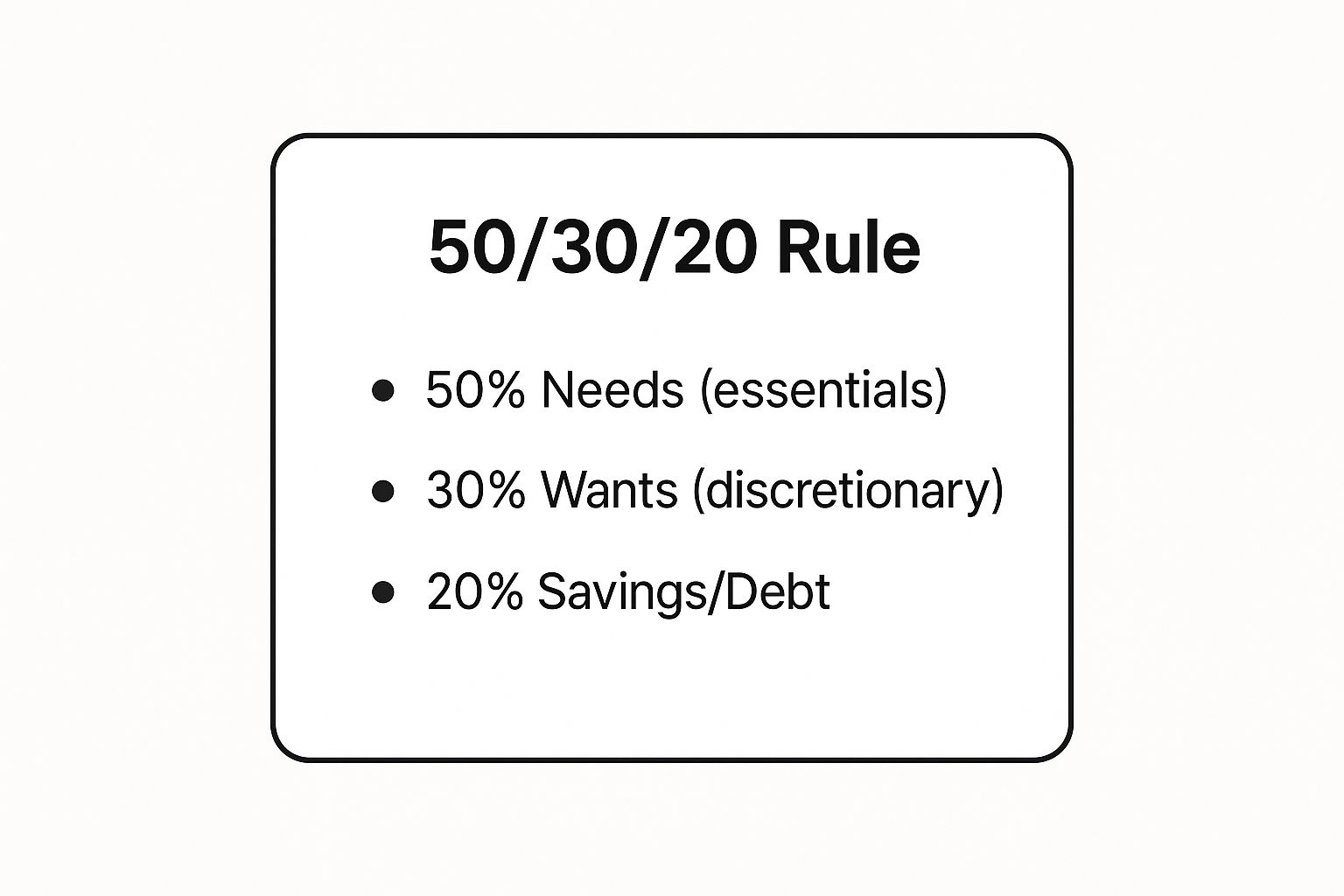

1. 50/30/20 Rule

The 50/30/20 rule is one of the most popular and straightforward budgeting tips for families looking for structure without excessive complexity. Popularized by Senator Elizabeth Warren and her daughter, Amelia Warren Tyagi, this framework provides a clear roadmap for allocating your after-tax income. It simplifies financial decisions by dividing your money into just three core categories, ensuring a healthy balance between obligations, personal enjoyment, and future security.

The core principle is to allocate your take-home pay as follows:

- 50% for Needs: This is the largest portion, dedicated to absolute essentials. This includes housing costs (mortgage or rent), groceries, utilities, transportation to work, insurance, and minimum debt payments.

- 30% for Wants: This category covers all discretionary spending. Think of dining out, family vacations, entertainment subscriptions like Netflix, hobbies, and new gadgets.

- 20% for Savings and Debt Repayment: The final slice is dedicated to building wealth and financial resilience. This includes contributions to retirement accounts, building an emergency fund, and making extra payments on high-interest debt like credit cards or personal loans.

To help visualize this powerful budgeting framework, here is a quick reference guide.

As the breakdown illustrates, this method provides a balanced approach to managing your family's finances. By clearly defining where your money should go, you can avoid overspending in one area at the expense of another.

For a family earning $5,000 per month after taxes, this would mean allocating $2,500 for needs, $1,500 for wants, and dedicating a full $1,000 to savings and accelerated debt repayment. A crucial aspect of this rule is its flexibility. A single parent, for example, might find their needs closer to 60% during a tight month. They could adjust by temporarily reducing wants to 20% while keeping their 20% savings goal intact, demonstrating how the rule can adapt to real-life circumstances. To start, track your spending for a month to see your current ratios, then automate your 20% savings transfer to prioritize your financial goals first.

2. Zero-Based Budgeting

Zero-based budgeting is a highly intentional and hands-on method, ideal for families who want complete control over where their money goes. Popularized by financial experts like Dave Ramsey, this system requires you to give every single dollar a job, ensuring that your income minus your expenses equals zero at the end of the month. It forces you to be proactive with your finances, rather than passively wondering where your money disappeared.

The core principle is to plan for every dollar of your take-home pay before the month begins:

- Income - Expenses = Zero: You start with your total monthly income and then subtract all your planned expenses. This includes savings, debt payments, and spending until nothing is left unassigned.

- Prioritize Needs First: Begin by allocating funds to essential categories like housing, utilities, groceries, and transportation.

- Assign Every Remaining Dollar: After covering needs, you assign the rest of your income to savings goals, extra debt payments, and discretionary spending categories like entertainment or dining out.

This method’s power lies in its detailed planning, which helps prevent overspending and ensures your financial goals are treated as non-negotiable expenses. It requires a detailed plan for your money, which can be a powerful tool for curbing impulse buys and staying on track.

For a family earning $6,000 per month, a zero-based budget might look like this: $2,000 for housing, $800 for groceries, $400 for transportation, $300 for utilities, $500 for savings, $500 for extra debt payments, $200 for entertainment, and so on, until all $6,000 is accounted for. This method is particularly effective for military families who need to adjust their budgets for fluctuating incomes during deployments. To start, use a budgeting app like YNAB or EveryDollar to simplify tracking. List all your fixed expenses first, then allocate funds to variable spending categories, and remember to include a "miscellaneous" category for unexpected small costs. Reviewing and adjusting the budget weekly during the first month is crucial for success.

3. Envelope Method

The Envelope Method is a time-tested, cash-based system that offers a tactile and highly visual way to manage spending, making it one of the most effective budgeting tips for families aiming for strict discipline. Popularized by personal finance expert Dave Ramsey, this approach forces you to physically see where your money is going. By allocating a set amount of cash into labeled envelopes for variable spending categories, you create a hard stop once the money is gone, eliminating the risk of accidental overspending common with credit or debit cards.

The system works by budgeting your discretionary spending for the pay period and dividing that cash into physical envelopes. Key categories for families often include:

- Groceries: A dedicated envelope to cover all food and household supply purchases for the month.

- Dining Out: A separate fund for restaurants, takeout, or coffee shops to prevent it from eating into the grocery budget.

- Entertainment: Cash set aside for family activities like movie tickets, bowling, or event admissions.

- Personal Spending: Small individual allowances for each family member to spend as they wish.

This method’s power lies in its psychological impact. Swiping a card feels abstract, but handing over the last $20 from your "Dining Out" envelope makes the financial consequence immediate and real.

As the video demonstrates, this system creates tangible boundaries. For example, a family might allocate $600 for groceries and $150 for entertainment. If the entertainment envelope is empty two weeks into the month, it means finding free activities until the next payday. It's a fantastic tool for teaching older children and teenagers financial responsibility; giving them envelopes for clothing or social activities provides a hands-on lesson in managing limited resources. A practical tip is to combine this with automation: have fixed bills and savings goals paid automatically from your bank account, and use the cash envelopes only for the variable spending categories you want to control. For those who prefer digital tools, apps like Goodbudget digitize the envelope concept for online spending.

4. Pay Yourself First

The "Pay Yourself First" method is a powerful and proactive budgeting strategy that flips traditional spending on its head. Instead of saving what's left over after all expenses are paid, this approach treats your savings and investment contributions as the most critical "bill" you have. This mindset shift, championed by financial experts like George S. Clason and David Bach, is one of the most effective budgeting tips for families aiming to build long-term wealth and financial security systematically.

The core principle is to allocate a portion of your income to your financial goals immediately after getting paid, before you even begin to pay for housing, groceries, or other bills.

- Prioritize Savings: The first transaction you make on payday should be a transfer to your savings, retirement, or investment accounts. This ensures your future is never an afterthought.

- Live on the Remainder: After you have paid yourself, the remaining money is what you use to cover all your monthly needs and wants. This forces you to live within your means while your savings grow automatically.

- Builds Discipline: This method removes the temptation to spend money earmarked for savings, automating good financial habits and making wealth accumulation a consistent, effortless process.

To help you visualize how this works, consider a family with a monthly take-home pay of $6,000. They decide to "pay themselves first" by allocating 15% to their financial goals.

As the chart shows, the priority is on future growth. This family would immediately transfer $900 ($500 to retirement, $250 to an emergency fund, and $150 to a child's college fund) on payday. They would then use the remaining $5,100 to manage all their other expenses for the month. This simple but profound shift ensures they are consistently building their nest egg. To get started, set up automatic transfers from your checking to your savings accounts scheduled for every payday. Even starting with a small amount, like 5% of your income, can build powerful momentum toward achieving your family's financial dreams.

5. Family Budget Meetings

Establishing regular family budget meetings is one of the most powerful and collaborative budgeting tips for families aiming to build teamwork and financial literacy. Popularized by financial educators like Dave Ramsey, this practice transforms budgeting from a solitary chore into an inclusive family activity. It creates a dedicated time to discuss financial goals, review progress, and make collective decisions, ensuring everyone is aligned and working toward the same objectives.

The core principle is to foster open communication about money. This approach helps demystify finances for children and gives every family member a voice, which can increase buy-in and reduce money-related conflicts.

- Transparency: Everyone gets a clear picture of the family's income, expenses, and savings goals. This eliminates guesswork and helps older children understand the real-world costs of running a household.

- Shared Ownership: When kids and partners have input on financial decisions, like choosing a vacation destination based on a savings goal, they become more invested in the outcome and more willing to help.

- Education: These meetings are a practical, hands-on classroom for teaching valuable money management skills, from delayed gratification to the importance of saving.

By making financial discussions a normal part of family life, you build a foundation of trust and teamwork. This method ensures that budgeting is a shared responsibility rather than a burden on one person.

For instance, a family might hold a 30-minute meeting on the first Sunday of each month. They could review the past month's spending against their budget, celebrate hitting their goal of putting an extra $100 toward their vacation fund, and discuss upcoming expenses like a child's school field trip. An essential part of this practice is its adaptability. A quick, 15-minute weekly check-in might work better for busy families to simply review upcoming bills and planned spending. The key is consistency, not length. To get started, schedule your first meeting, keep it positive and brief, and use a simple visual aid like a whiteboard to track a specific goal, making it an engaging and effective routine for the whole family.

6. Meal Planning and Bulk Buying

A strategic approach to food spending is one of the most effective budgeting tips for families, and it hinges on the powerful duo of meal planning and bulk buying. This method involves planning your family’s meals in advance, typically on a weekly or bi-weekly basis, and purchasing the necessary ingredients in larger quantities or during sales. By eliminating impulse buys and reducing food waste, families can gain significant control over their grocery budget, often one of the largest flexible spending categories. This proactive strategy not only cuts costs but also simplifies the daily question of "what's for dinner?" and encourages more nutritious, home-cooked meals.

This method transforms grocery shopping from a reactive chore into a calculated financial decision. The core idea is to create a meal calendar and a corresponding grocery list before you ever set foot in a store. This allows you to leverage sales flyers and seasonal produce, building your menu around the most affordable items available. Paired with bulk buying of non-perishables and freezable items like meat and bread from wholesale clubs like Costco or Sam's Club, you can lock in lower per-unit prices on staples your family uses regularly. This combination ensures you have a well-stocked pantry and freezer, ready to support your planned meals without last-minute, expensive trips to the store.

To put this strategy into action, consider these tips:

- Plan Around Sales: Before creating your weekly menu, review your local grocery store's weekly ad. Build your meals around proteins and produce that are on sale.

- Embrace Batch Cooking: Dedicate a few hours on a Sunday to batch cook core ingredients. For example, cook a large batch of chicken, ground beef, or quinoa to use in different recipes throughout the week.

- Invest in Storage: Good quality, airtight food storage containers are essential for keeping batch-cooked meals and bulk ingredients fresh, preventing waste and saving money.

- Create a Master List: Organize your grocery list by store layout (e.g., produce, dairy, frozen foods) to make your shopping trips more efficient and less prone to impulse purchases.

The financial impact can be substantial. For instance, a family that consistently spends $200 per week on groceries could realistically reduce their bill to $150 or less by sticking to a well-researched meal plan and buying staples in bulk. Over a year, this translates to over $2,600 in savings that can be redirected toward other financial goals, like paying off debt or saving for a vacation. By turning meal preparation into a planned activity, you not only optimize your food budget but also reduce stress and promote healthier eating habits for your entire family. For a deeper dive into controlling your food expenses, you can explore more techniques for budgeting for groceries on findtoptrends.com.

7. Automated Bill Payments and Savings

Automating your finances is one of the most effective budgeting tips for families aiming to reduce stress and build consistent financial habits. This "set it and forget it" approach involves setting up recurring, automatic payments for your regular bills and scheduled transfers to your savings accounts. Promoted by financial advisors and enabled by modern banking apps, this system removes the manual effort and mental load of managing finances, ensuring obligations are met on time and savings goals are consistently funded.

The core principle is to leverage technology to enforce financial discipline. By automating, you pay your most important financial obligations and yourself first, right after your paycheck lands.

- Automated Bill Pay: This handles recurring expenses like your mortgage or rent, utilities, car payments, and insurance premiums. Setting this up eliminates the risk of missed payments, late fees, and potential damage to your credit score.

- Automated Savings Transfers: This is the cornerstone of building wealth. You schedule regular, automatic transfers from your checking account to various savings vehicles, such as an emergency fund, a retirement account, or a college fund for your children. This treats saving as a non-negotiable bill.

By making these processes automatic, you remove the temptation to spend the money elsewhere. It simplifies your budget by ensuring that essential payments and savings goals are handled before you even look at your discretionary spending money. This powerful strategy aligns your actions directly with your long-term financial priorities.

For example, a family can schedule their $1,500 mortgage payment to be sent on the 1st of the month and set up an automatic transfer of $300 to their emergency fund on the 2nd, the day after their main payday. This guarantees progress on their goals without requiring daily attention. A key tip is to always maintain a small buffer in your checking account to prevent overdrafts from unexpected timing issues. It's also wise to review your automated transactions monthly to ensure accuracy and adjust as needed, a practice that pairs well with other smart financial habits. If you're interested in refining your spending further, you can explore more ways on how to shop smarter. By putting your financial plan on autopilot, you can focus more of your energy on your family and less on managing bills.

7 Family Budgeting Tips Comparison

| Budgeting Method | Implementation Complexity 🔄 | Resource Requirements ⚡ | Expected Outcomes 📊 | Ideal Use Cases 💡 | Key Advantages ⭐ |

|---|---|---|---|---|---|

| 50/30/20 Rule | Low — simple percentage allocation | Low — basic tracking tools | Balanced spending and savings | General family budgeting, beginners | Easy to understand; flexible; promotes savings |

| Zero-Based Budgeting | High — requires detailed monthly planning | Medium — budgeting apps helpful | Maximized financial awareness; waste reduction | Families needing tight control on every dollar | Eliminates waste; prioritizes goals |

| Envelope Method | Medium — physical/digital cash handling | Low to Medium — cash or digital envelopes | Prevents overspending; controlled spending | Cash users; families teaching kids budgeting | Tangible spending control; teaches discipline |

| Pay Yourself First | Low to Medium — automate savings first | Low — automated transfers needed | Consistent wealth building; emergency fund growth | Families focused on savings and investment | Builds savings habit; reduces temptation |

| Family Budget Meetings | Medium — requires regular scheduling | Low — time and participation | Improved communication; shared financial goals | Families wanting transparency and education | Enhances communication; teaches money management |

| Meal Planning and Bulk Buying | Medium — requires planning and inventory | Medium — storage space and time | Reduced grocery costs; less food waste | Families aiming to lower food expenses | Saves money and time; promotes healthy eating |

| Automated Bill Payments & Savings | Low — set and forget automation | Low — online banking setup | Avoids late fees; consistent saving | Busy families managing multiple bills | Reduces stress; ensures on-time payments |

Building Your Family's Blueprint for Financial Success

Navigating the financial landscape of family life can feel complex, but it doesn't have to be overwhelming. As we've explored, creating a sustainable financial future is less about rigid restriction and more about intentional design. It's about building a blueprint that aligns with your family's unique values, goals, and rhythm. The key takeaway from these budgeting tips for families is that there is no single "perfect" system. Your ideal approach might be a blend of several strategies.

Perhaps the structure of the 50/30/20 Rule provides the clarity you need to categorize spending, while the tactile nature of the Envelope Method helps control discretionary purchases like dining out or entertainment. For families seeking total control over every dollar, Zero-Based Budgeting offers unparalleled precision. The most crucial element, however, is consistency. Financial success is built through small, repeated actions over time.

From Theory to Reality: Your Actionable Next Steps

The journey to financial empowerment begins with a single step. Don't feel pressured to implement everything at once. Instead, choose one or two strategies that resonate most with your family and commit to trying them for a month.

Here’s a simple plan to get started:

- Schedule Your First Family Budget Meeting: Put it on the calendar this week. Use this time to discuss shared financial goals, not just to review past spending. This transforms budgeting from a chore into a collaborative project.

- Automate One Thing: Start by automating your "Pay Yourself First" contribution to a savings account, no matter how small. This single action builds a powerful habit and ensures your future is always a priority.

- Plan a Week of Meals: Dedicate an hour to meal planning. This simple act can drastically reduce food waste and cut down on expensive, last-minute takeout orders, directly impacting your budget's bottom line.

The True Value of a Family Budget

Mastering these concepts goes far beyond simply balancing a spreadsheet. When you actively manage your finances together, you are teaching your children invaluable lessons about responsibility, delayed gratification, and teamwork. You are replacing financial anxiety with confidence and clarity. A well-managed budget is a tool that empowers you to say "yes" to the things that truly matter, whether that's a family vacation, a down payment on a home, or a debt-free future. You are not just crunching numbers; you are designing the life you want to live and building a legacy of financial security for generations to come.

As you implement these strategies and look for ways to make your money go further, let us help you find the best value on your purchases. Explore FindTopTrends to discover curated deals and insightful shopping guides on everything from family essentials to the latest tech. Our platform is designed to help budget-conscious families like yours shop smarter and save more, making it easier to stick to your new financial plan.

Leave a comment